You found health insurance and it’s cheap as chips––great! Now you can sit back and relax, knowing you’re covered. Or can you?

Don’t be too quick to call it a done deal. Cheap health insurance isn’t cheap when it ends up costing you your life’s savings because you’re not covered (even though you thought you were).

I talked to Andy Williams, Insurance Broker and Founder of CNX Insure in Chiang Mai, and key sponsor for the Chiang Mai Expats Club. I got the scoop on what really happens with those “cheap” insurance policies. This has personal importance for me because I fear the policy I purchased earlier this year, before I investigated more deeply, falls into the “cheap” category. If you are living in Chiang Mai it will be relevant to you also.

The first thing that comes to mind when we hear the word cheap relates to cost, and when we’re talking about expat health cover, inexpensive is an attractive feature. It’s enough to make anyone jump on the most bargain-basement choice for health insurance, especially in Thailand, which saw 22,248 traffic accidents in 2019.

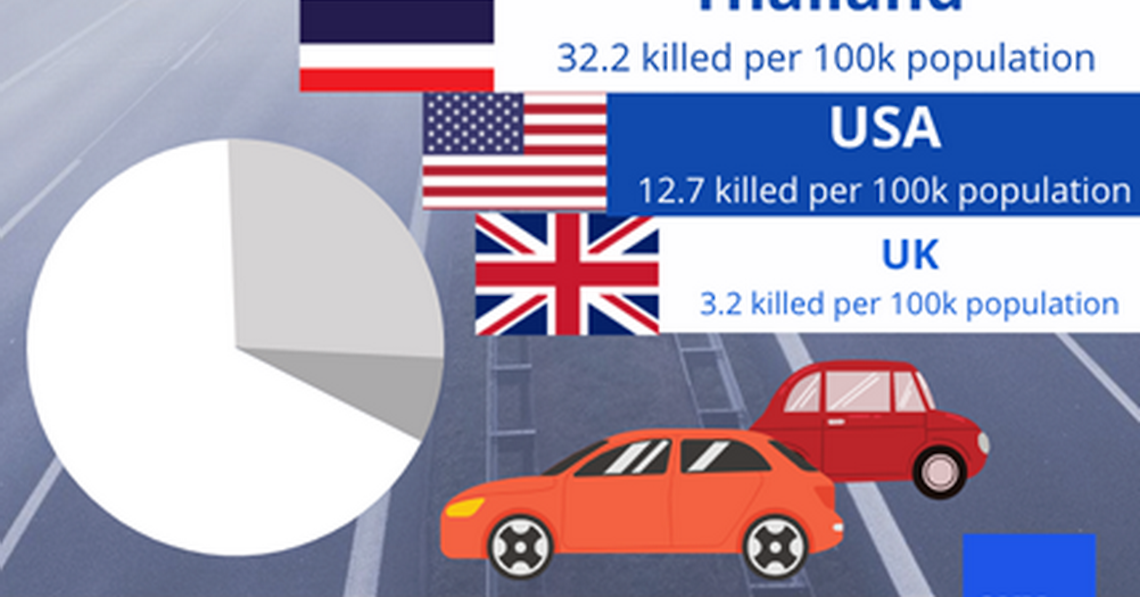

If you’re curious about how that measures against the UK and the US, check out these stats:

Number of Road Traffic Accident-Related Deaths Per 100k People

Thailand 32.2 z

UK 3.2

US 12.7

(2019 data from WHO)

Although shocking, it’s no surprise given that the risk of death due to traffic accidents is three times higher in poorer countries than in more affluent nations (source). Chiang Mai province also has one of the highest rates of traffic accidents. A mere three days into 2020, the province reported the second-highest number of death-related incidents––sixteen people (source). That’s more than five people a day.

Is cheap health insurance worth the risk?

So, let’s unpack the word cheap, shall we? Because there’s far more to that word than “budget-friendly.”

Recall the last time you strolled through a market looking for a t-shirt. Options, upon options, upon options. Racks and stacks of t-shirts beckon the budget buyer. But you know as well as I do that not all Thai-made t-shirts are equal. Some are made with low-grade “cotton.” Others have peculiarly angled seams. The odd t-shirt dons a fake logo, positioned upside for good market measure. That’s why those t-shirts are 50 baht instead of what they should cost. It sees one wash cycle, and the whole thing falls apart. You know what all that equates to, right? Cheap. In short, the t-shirt doesn’t do its job, and you just wasted your money, and you still need a t-shirt.

Now imagine making the same cheap choice with health insurance in Chiang Mai. For whatever reason, nature chooses to run you through the wringer with a heart attack, road traffic accident, or a life-threatening virus (heaven forbid, by the way). You end up in hospital through no fault of your own only to find out your health insurance policy doesn’t cover your medical costs. Don’t you wish you’d paid more so that your insurance could do its job?

Let’s remember something critical: we’re talking about health cover, folks, which is that handy little policy that may determine whether you live or die. Or end up in financial ruin. It sounds ghastly and harsh, I know, and that’s intentional. As an insurance broker in Chiang Mai offering private and group health cover, Andy reports seeing more instances than he cares to remember of lives turned upside down and inside out because people lacked adequate health insurance.

There isn’t a time more critical than now, during this COVID pandemic that has no foreseeable end in sight, to take a longer, stiffer look at the specifics and subtleties of health insurance policies. Furthermore, anticipating what surprises might be lurking inside a seemingly cheap policy is crucial. And––a word of advice from an expert in the industry, and my own personal experience––if you have to do that, keep looking. Transparency is key; there should be no lingering doubts in your mind about what your policy covers––and more importantly––doesn’t cover.

Andy shared a cringe-worthy story that exemplifies the heart of the matter:

He met a Harley Davidson member who was hospitalised for life-threatening injuries resulting from a road accident. He’d ended up in Chiang Mai Ram Hospital with broken legs and arms, a punctured lung, a fractured back, and a medical bill amounting to 4 million Baht. That’s over 92 thousand Pounds, or 128 thousand US dollars. Frightening. Most of us don’t have that kind of disposable cash lying around waiting for a tragic event to occur. Even if you do, I imagine you’d rather be spending it on other things (that’s a lot of good-quality t-shirts!).

Following his accident, a group of his fellow biker buddies, realising they were dreadfully underinsured, came to see Andy. They slapped their policies down on his desk, desperate. They’d paid 25K baht to some low-rate insurance company for what seemed like a comprehensive policy, except that it covered only up to 500K Baht of potential claims. I don’t have to point out what a hefty sum they would have had to pony up had it been one of them in that accident.

Those biker guys spend the majority of any given day facing the risk of road rash. And if you’re jettisoning that example as inconsequential to you because you don’t drive a scooter, car,

moped, or bicycle, then consider that you’re putting your life in the hands of a Grab or reckless tuk tuk driver and can be hit through no fault of your own whilst simply walking down the street. And that’s just traffic accidents.

Andy also described cases in which the victim of a heart attack or other life-threatening health event discovered only when they faced the operating table that their policy didn’t cover the required medical procedure. It goes without saying that’s an inconveniently timed discovery. Had they known in advance that their policy was inadequate, they might have chosen differently.

The reality is that anything can happen to anyone at any time, and our current circumstances help exemplify that disturbing fact. COVID-19 has raised the importance of health coverage to an unprecedented level. Not only can this virus get anyone it wants, the Thai government now requires a minimum of 100K health coverage plus COVID insurance for any location-independent foreigner who wants to enter and settle down in Thailand.

Why do people choose cheap insurance?

Reduced cost isn’t the only reason many people reach for cheap insurance.

In many cases it’s just more convenient. And let’s be honest––researching and buying an insurance policy is nothing short of a hassle. The terminology alone confuses even the best of us. We want to get it wrapped up quickly, just for peace of mind’s sake. I’m certain I’m not the only one who feels this way!

Be warned that there are loads of sneaky, if not scammy, local or international insurance companies in Chiang Mai waiting to pounce on just that sort of convenience-fixated victim. Some of these companies make buying a policy easy and straightforward by not requiring you to complete a medical assessment or questionnaire.

Those companies don’t ask about your medical history at all, which is to say they entirely disregard any pre-existing health conditions. That’s a relief for many people who feel they’re off the hook not having to disclose their current state of health or medical history. I don’t know about you, but I imagine a four million baht medical bill is a bit more inconvenient than just doing the homework in the first place.

As Andy said, rather bluntly: “You don’t want to have your medical history assessed on the operating table.” I couldn’t agree more.

I imagine there’s a sneaky psychological explanation behind people buying a cheap policy too. No one really thinks it’s going to happen to them; we’re all invincible after all, right? (I certainly was, until I realised I wasn’t). So maybe buying a cheap insurance policy just feels like we’ve

done our due diligence, the same way wearing a Fitbit makes us feel like we’ve already done the workout? Certainly a point worth pondering.

International, local, or group insurance?

Insurance policies offer a wide range of options, and that makes deciding what you need tricky business. Some only cover in-patient treatment. Extras may include, but aren’t limited to, out-patient medical services, vision, and dental. That applies to both local and international insurance companies.

In Andy’s professional opinion, international is generally the safer choice. He explains why:

“In a situation where there are no pre-existing conditions and someone has a heart attack, an international company would cover your claim without penalty. With local insurance, the equivalent policy’s premiums would double or even triple. That’s why I often recommend choosing an international provider and opting for a higher level of coverage with a deductible.”

While some people find the deductible discouraging because it means having to pay out of pocket for minor medical services, it means that you don’t have to pay when major medical services threaten your financial security (amputations don’t come cheap).

Get insured, not surprised…

Don’t take a chance with cheap insurance, the high-cost of low-rate health cover just isn’t worth the financial risk––and that’s as much advice for myself as it is a suggestion for you. Get good, reputable advice from a well-known broker and someone who speaks the language––it’s essential for negotiating the matrix of medical and legal terminology.